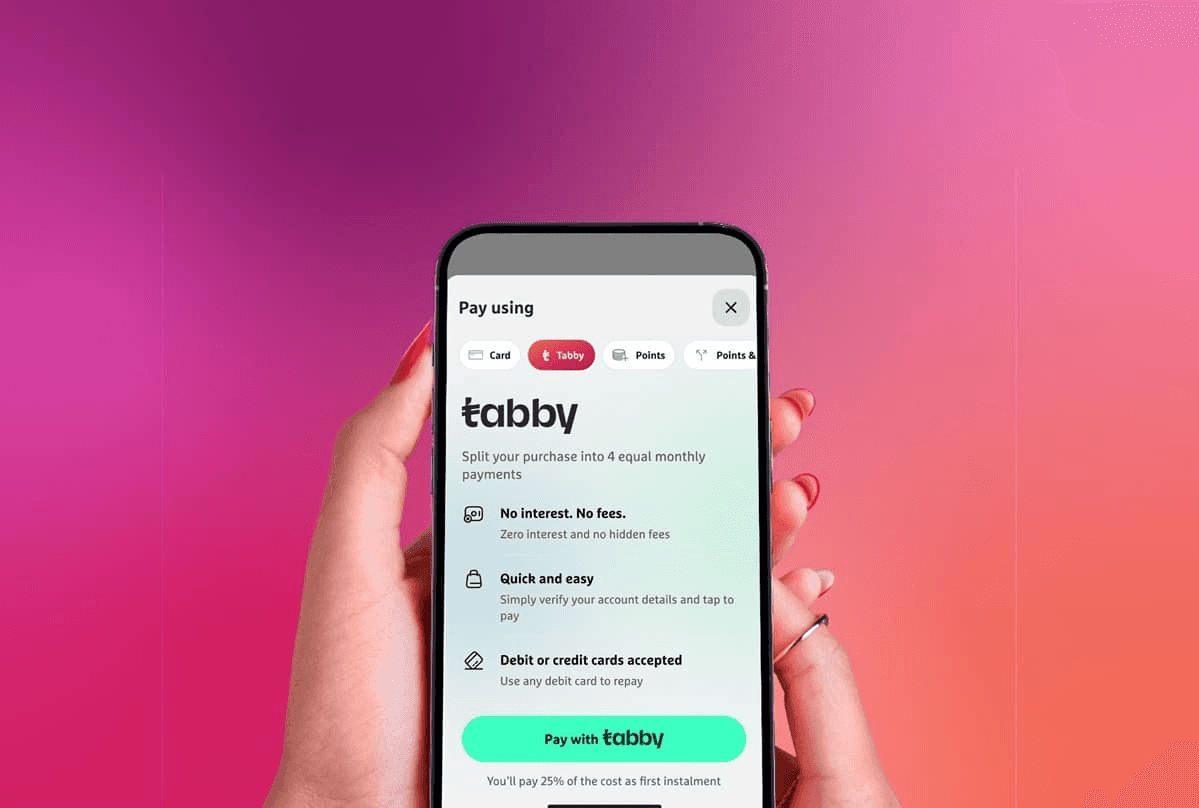

It was a busy Friday afternoon at Mall of the Emirates when Reem spotted the perfect pair of designer sunglasses—only “Pay in 4” at checkout stood between her and a spontaneous splurge. With a few taps in the Tabby app, she split the AED 1,000 cost into four interest-free installments, knowing her salary wouldn’t stretch unfairly. For millions of Gulf shoppers like Reem, Tabby’s buy-now-pay-later model has transformed the thrill of discovery into manageable payments—no credit cards, no hidden fees, and fully Shariah-compliant.

Founded in 2019 by serial entrepreneur Hosam Arab and technologist Daniil Barkalov, Tabby was born from a simple insight: despite soaring e-commerce growth, credit-card penetration in the GCC lingered below 20 percent, leaving many consumers dependent on cash or wary of interest-based loans. Arab’s experience scaling Namshi revealed e-commerce’s promise stifled by payment hurdles. By offering zero-interest installments that align with Islamic finance principles, Tabby bridged cultural and financial divides, giving shoppers ethical flexibility while merchants saw conversion rates climb.

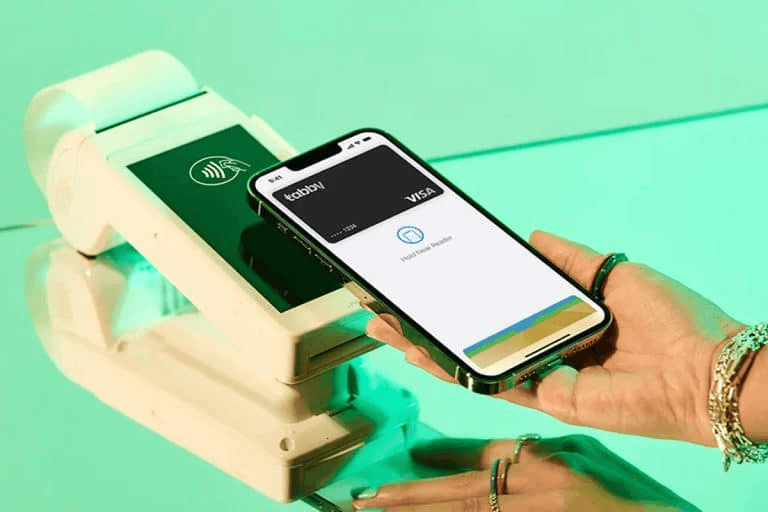

Tabby launched with a straightforward “Pay in 4” option—four equal payments due every two weeks—but quickly evolved. In late 2023, the acquisition of Saudi digital-wallet provider Tweeq introduced virtual and physical Tabby Cards, vaulting the company into neobank territory. Subscribers to Tabby Plus enjoy extended repayment windows and exclusive promotions, while Tabby Shop—a curated deals marketplace—hosts over 2 million products, making the app both a checkout solution and a discovery engine. To protect consumers, Tabby Care adds a buyer-protection guarantee, reimbursing faulty or undelivered items.

Tabby’s traction has been staggering. As of Q1 2025, annualized transaction volumes exceed US $10 billion, and registered users top 10 million, with 30 000 active merchant partnerships spanning fashion, electronics, travel, and dining a threefold increase since 2022. Its Series E funding in February 2025—US $160 million at a US $3.3 billion valuation—cemented Tabby as the MENA’s most valuable fintech, led by Blue Pool Capital and Hassana Investment Company alongside STV and Wellington Management.

For shoppers, Tabby delivers convenience and control. In Riyadh, a university student uses Tabby to split textbook bills, avoiding cash shortages. In Cairo, a young graphic designer funds her first MacBook Pro with Tabby’s four-installment plan—sidestepping high-interest credit cards entirely. Merchants, too, reap rewards: brands report 20–30 percent higher average order values and 15 percent lower cart abandonment when Tabby is offered at checkout. Major retailers—from Adidas and IKEA to regional startups—integrate Tabby’s SDK to tap into its “mature, credit-shy” consumer base.

Despite its success, Tabby faces headwinds. The UAE and Saudi Arabia have tightened BNPL regulations to guard against consumer over-leverage, requiring lenders like Tabby to implement spending caps and mandatory affordability checks. Competition has intensified: Tamara and Spotii vie for market share, and Tabby’s exit from Pakistan in June 2025—citing economic headwinds—underscored the difficulty of sustaining BNPL models in hyperinflationary contexts. To stay compliant and competitive, Tabby has invested heavily in AI-powered credit scoring, real-time risk-monitoring, and financial-literacy initiatives for users.

Tabby’s leadership envisions a “digital financial ecosystem” beyond BNPL. The integration of Tweeq’s e-wallet and card services moves Tabby toward embedded finance: micro-loans for SMEs on its marketplace, wealth-management features, and cross-border remittances. Upcoming pilots include “MaaS subscriptions” bundling rides, micro-mobility, and deliveries, and a blockchain-based credentialing system for verifiable transaction histories. These innovations aim to lock in user engagement and diversify revenue streams beyond transaction fees, positioning Tabby as a true super-app for finance and lifestyle.

Beyond balance-sheets, Tabby measures impact in financial inclusion. By early 2025, over 1.5 million previously unbanked users accessed credit for the first time, fueling home appliance purchases, education costs, and emergency expenses without predatory interest. Training programs certify local partners in responsible lending practices, while user-friendly interfaces and multi-dialect support lower digital-literacy barriers. Tabby’s “Fair Finance” report reveals 77 percent of users plan to use BNPL for essential spending—underscoring its role as a tool for empowerment, not just convenience.

From a ride-hailing spin-out to a US $3.3 billion fintech leader, Tabby’s trajectory encapsulates the Gulf’s digital renaissance. By marrying cultural sensitivity—Shariah compliance and Arabic-first design—with global fintech best practices, Tabby has rewritten how Gulf consumers pay and how merchants sell. As it deepens its fintech suite with lending, insurance, and banking services, Tabby stands at the forefront of a new era: one where access to flexible, ethical finance is no longer a privilege but a right, available to every shopper across West Asia. And for that savvy mall wanderer Reem, a simple tap on Tabby is the key to financial freedom—today, tomorrow, and beyond.